This analysis will be using the underlying work of Roger Stern's article released online at 26 DEC 2006 on The Iranian petroleum crisis. The article is released to Open Access before publication.

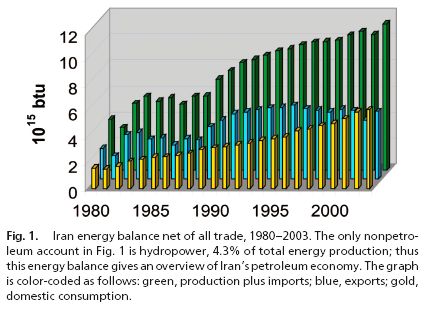

On of the misconceptions about the Middle East is that it is a region not only with lakes of oil, but regimes wishing to maximize the use of such lakes. These are misconceptions on two counts: 1) not all lakes are economically equal, and 2) most regimes are out to maximize income, not maximize production. These two things, taken as a basis for work and reasonable, based on the attitudes of the regimes involved, then let a closer examination of Iran and its oil reserves to be done. The article starts with an overview of the petroleum sector of Iran. Here the basic understanding is that some of what is produced goes for internal use, and the rest for export, thus a balance between production and consumption must be maintained for steady export. Now, no proper study of such a thing can be done without a colorful graph and they do provide a nice one in 3D, showing the total quantities of each. I, personally, would have preferred a line graph with production and then consumption overlayed with the difference between them being exports as it is more visually appealing and a better rendition of the data. Be that as it may, here it is: What is seen from this, then, is that save for a drop during the war with Iraq, Iran has had a steady increase in production that has been plateauing since the late 1990's. There have been upticks over the last few years, but also notice that there are subsequent declines, this the article attributes to some better oil recovery techniques on older fields, opening of old oil rigs damaged in the Iraqi war, and not continuous increases in production or new production coming online.

What is seen from this, then, is that save for a drop during the war with Iraq, Iran has had a steady increase in production that has been plateauing since the late 1990's. There have been upticks over the last few years, but also notice that there are subsequent declines, this the article attributes to some better oil recovery techniques on older fields, opening of old oil rigs damaged in the Iraqi war, and not continuous increases in production or new production coming online.

If you are in charge of the Iranian regime, however, the greatest worry is that set of lines in gold which is domestic consumption. That has been on a continual, steady increase even *with* the war with Iraq and has not abated, year on year. As trendlines go, these point to a crossing at some point in the future if there is nothing done to either increase consumption or decrease demand. That center bar is exports and as consumption increases and production plateaus, exports decrease as a result. Being a part of OPEC, however, Iran has export quotas to meet and has been missing them for the last 18 months, which Mr. Stern points to with interest as the only other time there has been a shortfall was during the war with Iraq.

Now, to understand an oil based export economy, you have to understand the processes behind the extraction and refining of oil, just in overview. I will not try to make this a fully encompassing review of that, but to at least get a good sketch of the ideas involved. Yes it is lengthy, no it is not a thorough review of the actual process.

First off is that when one starts to drill for oil, you expect to come up with some dry wells. This is still more of an art than a science, and doing a good analysis on sub-surface geological structures, finding ones with oil, finding ones with oil that have some porous rock, and finding ones with oil that have porous rock that allows pumping requires knowledge, skill and experience in the actual geology involved. To do this one studies actual outcroppings if they appear at the surface as a very first hand thing to see what you are dealing with. As structures can extend thousands of miles, a first, actual look at a possible containment rock strata may occur in another Nation or even, with continental drift, another continent. With that in hand you can then head over to a lab, thin section the rock and start killing your eyes for hours on a microscope counting crystals and grains, looking at spaces and then determining the 3d structure of the rock involved and determining how porous it is.

Things like shale may have plenty of oil in them, but it is locked into the granular structure of the rock itself. If there is not overt pressure and heat to force the less dense oil from the rock, it will just sit there, so plenty of oil in an oil shale may be right near the surface, but your only option is to mine down to it. Some structures may have a great porosity and even have an oil shale or other oil bearing formation that is under them, with enough depth to cause the necessary pressure to let the oil move through it if the temperature is right. Typically a sandstone, but many other rock types can also fit this bill based on grain types, spacing and a host of other concerns. But, if that sandstone has multiple layers and one is relatively impervious to this movement, you will have a much lower entrapment of the oil than you would with a rock strata that had more uniform porosity.

Next up is a seismic survey of the area you suspect may have oil. This is done in the modern day mostly by 'shaker trucks' and going out and having them plunk down, shake a bit while you get the readings, then the truck raises, drives on a bit, plunks down again, shakes... almost all of this is done with GPS today, but back a few years ago you brought a survey team out first, put down lots of little flags and hoped a windstorm wouldn't take them all away. Then you throw all of that wonderful data into a computer with various software tools to get rid of noise, adjust incoming data waves based on rock density that is known and start to build up an idea of where the rock strata actually are. This, for a virgin field, can take a long time. What one likes to look for are domes or other formations that will act as a 'trap' for lighter oil and gas in a porous rock layer. So with the measurements of the depths of the layers you throw all of THAT into a computer and start doing your adjustments to remove surface elevation and get a real idea of what the subsurface looks like. In the old days that was sometime done with clay or sand and plaster and toothpicks and whatever else you could devise. Today a subsurface 3d modeling or graphing program will do that for you and let you twist and turn everything every which way.

Two years later and you are now at the point where you will dig your first test wells! Isn't this grand? If you have a suspected area with rock the right porosity, depth, pressure and so on, in an entrapment structure with known oil bearing strata beneath it, you can now actually drill a bore hole and not only get a core sample down to the expected depth of a well, but then put down other instruments to measure such things as density, fluids, and hydrocarbon emissions. Now, at this point once you finally get the core sample and start doing the data analysis you can find out a whole lot more, but the investment has just gone up to do this, too. You may get the core sample and find that the pressure has morphed the target layer to being semi-porous or even to being impenetrable. You may also find that you are not getting the exact same type of rock as you examined earlier, and find that it has changed its characteristics in that strata. Thus it may still be oil bearing, but the oil now adheres more to the granular structure rather than flow through the spaces due to changing in grain and space size. Do this at a few sites to get an idea of the actual strata changes and characteristics and then refine your calculations and do one or two more test drillings before you call in the big rigs.

At three or four years out you may *finally* analyze it all and realize that it 'looks like a reservoir' but the amount of pore space is so small that even modern steam technology isn't going to get a fair return on the investment. All the money spent by that point was for naught, though the company or Nation involved may file that for 'future use' when the technology gets better. But if everything has gone as expected, you may finally do the first real expensive work of getting a full rigging crew in and boring into the target area. This usually requires a more intense seismic survey, more subsurface mapping and so on.

You can find that even at this point, the well gets drilled, the core samples are spot on and you decide to fracture the pipe at the best calculated depth and you get *nothing*. Something just changed down there or you made a miscalculation or the oil bearing strata just isn't cooperating. Another hole can be done, but only for a really promising prospect, and most companies will do another 'just in case'. If all the folks working with you have done the best they can and nature has cooperated with you, then you can hope to get oil with a known and expected pumping rate. You have calculated the volumetric reserve space and now you have good predictions on just how long that field can produce at that rate. Large fields tend to get more wells drilled as the expected reserves go up in estimation.

The moment you begin pumping you begin the process of utilizing the reserve: you are taking oil and gas out of the reservoir. As the input of new oil into a reservoir is based on subsurface structures and conditions, it may prove to have somewhat greater reserves than expected. Or lesser. What is done is to give a minimum expected reserve size based on expected capacity and you go with that.

All of this gets shortened with known reserve areas, and, over time as more wells go in, a better idea of the entire field comes into view as more data populates the subsurface structure maps. Thus you get adjustments on expected reserve size even in fields that are well known and utilized.

Thus the main factors for starting up an operation are the upfront cost expenditures necessary to find the potential area, explore it, analyze it, do test wells, integrate that data and then actually put in the hard cash for a real well. That cost gets spread over the lifetime of the well itself and is a static cost onto which maintenance and overhead get added. But all of that gets added in to what actually makes it out of the system, which can be something rather less than what went into it.

Here the main obstacles are mostly physical: oil pipeline waste and leakage. Some problems also crop up with suspended sediments or with natural gas that was held in solution under pressure or with a high degree of brackish water mixed with the oil. Filtration, sorting and then piping that to a refinery will account for system loss. The natural gas, if the system is not set up for utilizing it, will be vented and flared off. When you go for oil, you also get natural gas as a result of it, because it, too, is a hydrocarbon. Brackish water, because of the pressures involved at depth, may be in suspension and then turn into steam or hot brine at the surface. Luckily it separates out pretty well and can be handled. Sediment is mostly handled through screens and this thing known as 'cleaning out the pipe'. Usually an automated, remotely operated vehicle, but often a man in a protective suit with high pressure hose/sand blaster/shovel/scoop/bags depending upon situation. Also, the entire affair will leak oil sooner or later and finding those holes and patching them or adjusting fittings is another headache. I got to hear about all of this in a seismic prospecting class so you don't have to!

Still, compared to the actual volumes and economic worth of the oil involved, this stuff is tiny in comparison, although the loss due to leaks and systemic inefficiencies (old equipment slowly breaking down and losing oil) is non-minuscule in the case of Iran. Most oil rich Nations don't let their equipment go to pot, and will hire foreigners to take care of it. You don't employ your own people because, if you did, they might get this silly notion that they could run it better than the Government could! Can't have that, now, can we?

So, from the Stern report we get the known depletion rate for Iran, as a whole, as 8% for the fields alone hich includes pipeline leakage and such, and an additional 2% due to domestic consumption, for a 10% decline in total exports (export decline rate). Mr. Stern cites 5-6% edr as a Global average, so 10% is indicative of something negative happening and, if that former oil minister he cites is correct and it is really on the order of 12%, then that amount left over for export is declining rapidly. Now most companies and Nations combat this by either opening up new wells, finding new ways to utilize their old wells, or seek to stem consumption. If the amount pumped goes up, year on year, then so long as it outpaces the increase in domestic use, there will be a continuous supply for export.

That said the cost to add to an existing field, as seen above, still has Marginal Cost to it, which must be calculated before figuring out if it is economical to do. That cost will be associated with the expected output and that which is then associated with the overall production rate so that an annual cost of investment can be determined. Yes, you plan on investment based on known reserves, some future exploration, and the amount of oil you want to export so as to keep ahead of domestic demand. While it is economics, it is *not* rocket science and has been done for decades if not a century or more for this and other industries. For Iran to keep its export amount steady, it must invest $2.7 to $3.2 billion/year in its petroleum infrastructure each and every year. This includes the amount necessary for simple infrastructure maintenance, which comes in around $1.6-1.9 billion/year.

Future demand and current and sustained capacity have assumptions built into them, and forecasting means that those assumptions have to be pretty close to what actually happens so you don't wind up with a disaster. For the last four years Iran has been investing enough to keep its current infrastructure going, but very little to upgrading and keeping up with additional production. Since Iran has only been investing $2.1 billion/year on average since 2004, it is seeing a significant shortfall on additional growth capability. If, however, they are expending more into growth, then infrastructure is getting shortchanged, and as they actually do have pipeline and refinery loss of petroleum, that is indicated.

Further, expected expansion on current fields is seen as optimistic and even if properly funded and put in place they will not come online until 2009-10 at earliest. And Iran's own ability has not been put to use since the 1978 revolution, so the one project that Iran is overseeing on its own has some question marks by it as to if it will be done right and economically. A major sticking point in this is one of the larger buyers of Iranian oil, Japan, holding Iran to its Nuclear Non-Proliferation Treaty and *not* supplying it with the funds to actually start these new expansions. So even the fully functioning old oil platforms that are brought on line, and one doubts the ability of Iran to get them into fully operational condition based on pipeline and refinery losses, will only raise the plateau by a smidgen while slow and steady draining of existing reserves will start to deplete those reserves until actual, total production starts to fall. Remember, starting a project *now* means additional capacity in 4 or 5 years, not tomorrow.

To further complicate things, the regime in Iran has instituted a 'buyback' system for oil production so as to keep foreign investors from 'owning' the wells which has caused much grief as the traditional 'share of the goods' concept now requires a cross-payment system between the producer and supplier. What this means is that a complex series of offers and agreements gets yanked by politics at the whim of the regime. Any international problems it has with any Nation can instantly have offers withdrawn, marked up or replaced with a lesser offer. This wrecks havoc on forecasting and ensuring a steady supply of production and has led to companies and Nations, beyond Japan, not doing any investment in the Iranian infrastructure. This started in 1998 with international pressure and has gotten worse over time, which means that the pipeline and refinery problems that are being seen are not 'point source' but systemic: point sources are related to individual events and happenings, systemic are year-in and year-out unaddressed problems.

With the loss of foreign support and investment, then, comes a loss of foreign expertise, management and training in the petroleum industry. Since the revolution, Iran has not led a successful major expansion plan on its own and could very well be incapable of bringing such a project online. Without foreign support, the regime then needs to rely upon interior knowledge, and that is demonstrated as lacking by those self-same infrastructure problems. To get to the problems one needs the knowledge and skills that can be provided by those with expertise. If Iran had the expertise, they would *not* have the problems.

That has led to the lack of secondary methods for oil recovery from existing fields from operating effectively which is slowly increasing the depletion rate of those fields upwards on an annual basis. For oil, as a whole, this is a worrying concern as an inefficient utilization of relatively inexpensive methods now, will cause a resorting to even more expensive methods for recovery sooner rather than later.

On the natural gas side, Iran has a problem of subsidized domestic use of natural gas and committing to large, foreign export contracts. Because the domestic market does not need to pay a market price, domestic use is expanding at a far higher rate than expected, to the point where actually having enough natural gas to meet foreign contracts is called into question. While trying to bribe its home population and curry favor with Asia in natural gas exports, the regime has suddenly found itself in a bind with inefficient recovery techniques for natural gas. This is so tearing at the regime, itself, that it is now trying to decide if it can actually export ANY natural gas within five years, not to speak of meeting contracts on it. Topping all of this off is that the best way to get more oil from existing fields is to inject natural gas INTO them so as to change fluid levels and allow additional extraction. Thus, natural gas is already being torn between domestic demand and trying to meet foreign contracts and then is no longer available for petroleum field maintenance and secondary production.

For refined products, such as gasoline, Iran has been subsidizing those, also. Again, the domestic market is treated to sub-sustainment level pricing, which allows for gas to go at a set, low price. What that returns is increased and heavy demand for said gasoline which then starts to outstrip domestic production of it. Foreign gasoline is more expensive to the public, but less expensive than refining it domestically as that system is not efficient to do so. Yes, by encouraging use and not maintaining the refineries for gasoline, Iran may be reduced to buying foreign refined gasoline of its own crude oil! And that resulting sticker shock to the Iranian populace will be hard and heavy as they are paying 34 cents per gallon and the open market price is in the $1.30-$1.50 range without additives and such for meeting emission standards. A sudden rise in Iranian gas prices by four to six times current amounts will have a decidedly negative impact upon their domestic economy.

So, while there is a 'sea of oil' under Iran, the 'sea of cash' is heading directly into the pockets of the regime. After minimal outlay into maintenance and now none into future expansion, Iran has a decided problem, just on that *alone*. This is further compounded by running a regime and market so hostile to foreigners, that they will no longer invest in Iranian petroleum or natural gas production as there is no way that a guarantee of future production can be assured. As this has been going on for some time the actual pipeline and processing infrastructure has started to lose its knowledge and support base and run less and less efficiently over time. This is seen in actual loss of petroleum in refineries so that a marked 3-4% of all petroleum is actually LOST just from field to finished delivery while most other Nations achieve so close to 0% as not to be funny. As crude and refined petroleum are the lifeblood of Iran, it is willing to lose 3-4% of that which will not reach any market, anywhere as it is lost to waste and inefficiency and unrecoverable. It is *not* stolen or hidden or sequestered: it is produced and LOST.

The domestic marketing of natural gas and finished products, like gasoline, have increased demand for both substantially, far out of line with normal economic expansion. These internal subsidies no longer gain any bonus for the regime, save a modicum of bought 'good will' for providing the cheap goods. What that has done is further make home refining uneconomical and marginalize their own refineries to the point where they may no longer be used for refining. On the natural gas side, increased consumption, both for home use and for electricity production, are removing a disproportionate stream of natural gas to pure use. As there has been no substantial increase in natural gas production, promises on that to buy good will with foreign markets is now coming into question. And without a substantial amount of natural gas to revitalize older oil fields, those oil fields lose additional production and may have to resort to more expensive oil recovery techniques which will further drive down the actual profit made on it. By removing the natural gas stream to a rapidly expanding domestic economy, Iran may have no ability to meet foreign contracts or to maintain actual crude oil production.

What is being seen is that the export capability for Iran in both crude oil and natural gas is in danger by the regime, which has used oil profits to fund terrorism and buy weapons, instead of investing in their 'cash cow' first. As domestic natural gas production is dedicated more and more to domestic use, and that use expands rapidly due to subsidies, the current plateau of oil production will start to dwindle rapidly within a decade. And as that goes, so goes exports as they are the difference between domestic consumption and total supply. When those two lines get closer, exports dwindle and contracts are no longer met.

When does that happen?

From the beginning of the article it is noted that for 18 months Iran has not met its OPEC export quotas. That is one of the most basic of futures to be met: the agreement amongst Middle Eastern States to ensure world crude oil supply. Iran is failing that.

So when you hear that 'Iran may threaten to cut off its exports' it may not be due to ANY outside activity at all. They may have simply run out of oil to export.

And that will happen far before those two lines meet as when a system that is complex like oil refining begins to decay, it indicates that the most complex part of a very complex interlocking system is already going to hell. When that part of the system cannot be maintained properly, even at a LOSS, which is the case now, there is then a leading indicator that the less sophisticated parts of the system, like pipelines, pumping stations, well-head pumps, separation facilities and so on, are also being run inefficiently. The expertise needed to run those is in the same league, but more distributed as that needed to run the refineries. Those are now seen as not running up to capacity, either.

The explosions and missiles and weapons that you see causing harm in Lebanon and Iraq that are supplied by Iran are doing far more damage to Iran's petroleum infrastructure than they can ever do to Lebanon or Iraq. They may be going off elsewhere, but the damage being done is at home where it is not only not being fixed, but being actively disregarded.

If Iran announces that they will *not* be expecting to let any liquefied natural gas contracts of a substantial amount or will be stopping existing contracts, then a first and mighty indicator will be seen.

If Iran buys gasoline or any other finished petroleum goods en mass and announces refinery 'problems' then that, too will be an indicator.

And in the next five years if Iran announces that it will be 'shutting off its oil to the world', that means that it is no longer producing enough to sell and that it can barely cover internal needs.

When I first heard of this article and what it portends, the indicators were shocking to me. The blatant disregard of modern economics and basic prudence in this field by a Nation so heavily dependent upon it is beyond amazing. Iran is slowly unraveling no matter *what* the price of a barrel of crude oil actually IS, they are slowly closing the gap between production and consumption on both sides of the equation. Trying to get old, inefficient equipment on the old maritime oil platforms up and running will in no way meet this need and may even draw off further resources from maintaining the current infrastructure.

Exactly how close is the Iranian petroleum system from collapse?

It is a metastable system with a heavy change bias to it. Internal collapse between 2012-19 is certain with current domestic market needs increasing and actual oil field production declining. And like many systems in decay the half-life is very important, because it is usually the inflection point for catastrophe: it is the point where a ship sliding to its side will suddenly capsize. It is the spell of bad weather for a year or two that can change lush cropland into dustbowls.

A point of no return.

28 December 2006

Iran's Oil Problem

Subscribe to:

Post Comments (Atom)

Supporting Friends and Allies

Supporting Friends and Allies

2 comments:

For some knowing that Iran has oil problem is shocking since the country is well known for having a great deposit of oil but if you will look deeper and understand the current situation there you’ll fully understand why. This article of yours explains the problem pretty well.

World Oil Prices

jazs07 - Since this article the Iranian regime has stopped subsidizing gasoline, which has put a major hole in the pockets of the population. For a few short weeks Turkmenistan stopped exporting natural gas to Iran which lead to shutdowns of service to much of the population in Tehran just to keep the bakeries going. What was involved was a delta between what Iran would pay for natural gas and what Europe would pay and Iran was successfully forced to pay more for natural gas.

Effectively Iran no longer has a reliable system of refining and is now depending on middle-men to supply refined products. Without even marginal expansion of its fields, the cash flow will soon dry up as domestic consumption causes a negative trade balance just to get refined products. That is not good. At some point the system collapses as Iran can't meet internal needs. The Green uprising was just the first hint of this.

Post a Comment